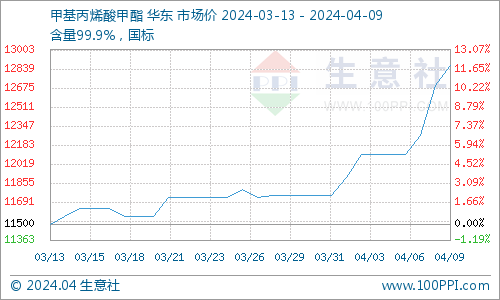

Before the Qingming Festival, the domestic MMA market ended at a high level, and the rally after the festival was even stronger, and the market offer directly rushed to more than 14,000 yuan/ton. As of April 9, the Shandong market MMA offer in the 14600-14650 yuan/ton spot can price, slightly higher offers have also been heard, compared with the end of March the market has increased by more than 1,000 yuan per ton.

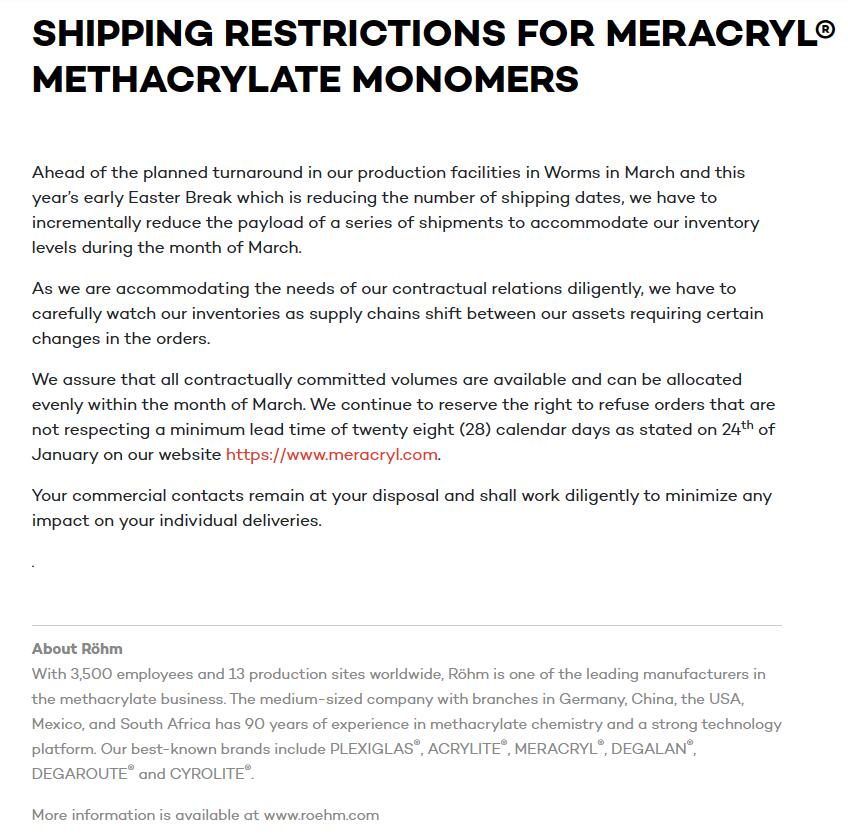

In Asia, tightened MMA supply continues to propel MMA prices upward by US$100~150 pmt in April. This increase is fueled by the ongoing surge in MMA demand from the USA and Europe, alongside escalating MMA prices in China and the struggles of most MMA plants with low inventory. In Europe, MMA production has been hindered by a rail strike in Germany and tensions regarding commercial ships, significantly disrupting the region’s supply of MMA and raw materials originating from East Suez. Many tankers have been compelled to take the longer and more costly route via the Cape of Good Hope or seek other alternatives options, thereby contributing to supply scarcity as facilities operate at reduced capacities. Additionally, on the first of March, RÖHM announced shipping restrictions for MERACRYL® methacrylate monomers. RÖHM assure that all contractually committed volumes are available and can be allocated.

In America, tight MMA supply is expected to remain limited till Q2, as several MMA plants have planned shutdowns or reduced production between Q1 and Q2. Additionally, logistic costs are expected to increased moving forward due to Asia-US freight costs, while wait times at the Panama Canal edge lower before May. The transportation demand through the Panama Canal has decreased to 24 authorized crossings pre day until at least April. It’s been reported that if the expected rain occurs in May, the canal plans to gradually increase daily shipping schedules, with the goal of returning to about 36 ships per day. Furthermore, the Fed has kept interest rates steady and continued to signal three rate cuts this year, providing some support for market demand. Converse, the militant group Islamic State in Khorasan (ISIS-K) claimed responsibility for the terrorist attack on Russia’s Saffron City Hall concert hall on 22nd of March, resulting in the deaths of at least 137 people and injuries to over 100 others. Russian President Vladimir Putin insists that Ukraine is somehow linked to the terrorist attack, which he believes will escalate the situation in the Russo-Ukrainian war. The Israel’s occupation of Palestinian territories, which began on the 19th of February, remains unresolved. As a result, geopolitical conflicts persistently keep the market on edge in Q2. Additionally, Argentina has been grappling with long-term inflation and a volatile exchange rate. After President Mirei took office, he allowed the peso to depreciate further, exacerbating the existing inflation, with the inflation rate soaring as high as 276%. On the market demand side, despite the high prices of MMA in Europe / America and the tight supply, most buyers are hesitant to commit to these high MMA offers. They argue that the increased cost of MMA can’t be passed on to end-user owing to persistently slow demand fundamentals. Consequently, MMA off-take in Asia and China remains to decline, prompting buyers to request that MMA prices remain rollover for April shipments. Looking ahead to May, the outlook for MMA supply remains tight and firm.

PRODUCTION

In Europe, the shift to tighter spot MMA has been reflected in the spot market, with prices levels now typically sitting at or above levels usually seen for contractual sales. The MMA production issue that affected the market balance in late June has been resolved, and it is now the additional demand that is providing continued support for MMA prices. Sellers and buyers are fully aware of the tighter market position and the restriction in sourcing derivatives from deep-sea locations. It’s been heard that RÖHM 225kpta MMA plant in Worms, Germany, is planned to shut down for maintenance between 11th to 17th of March. Moreover, after Mitsubishi Chemical Corporation reported that some of their existing Methyl Methacrylate(MMA) utilizes raw materials derived from biomass, RÖHM announced on 14th of March that customers have a choice at RÖHM: an extensive offering of sustainable products is available. This announcement indicates that the Worms and Wesseling production sites have received certification under the International Sustainability and Carbon Certification (ISCC) PLUS scheme. The sustainable product range is also continuously expanding. Selected products from all established brands, including PLEXIGLAS®, DEGALAN®, DEGAROUTE® and MERACRYL®, are already available with a reduced carbon footprint. These products, branded as proTerra, are based on a proportion of renewable or recycled raw materials. In the US, the upward movement in MMA prices, combined with a tight market, will give MMA sellers the upper hand in discussions and lead to an expected price increase. The MMA supply is expected to remain difficult in April owing to low inventory, which could keep supply security top priority. It’s been heard that the RÖHM MMA plant in Fortier, Louisiana, plans to shut down for maintenance in March. Additionally, the high spot acetone prices have driven up costs. MMA makers are monitoring feedstock availability, and hoping for some improvement in Q2, as it would lower input costs and boost MMA production. It’s been reported that MMA makers have announced an increase of 9¢~14¢ per pound between March and April. Additionally, while oversea logistics continues to impact imports, import from Asia are still limited as local production is curtailed and netbacks are higher in other regions. However, US domestics MMA prices are still cheaper despite price increases. In Asia, it’s reported that Singapore’s Sumitomo Chemical plans to shut down two units owing to muted market demand and high MMA costs. In Japan and Taiwan, it’s said that several MMA makers have cut or shut down their production rate in conjunction with the upstream acrylonitrile (AN) plant production cuts. South Korea and Thailand, averaging at 70~80%, are affected by upstream decreased run rate and high raw material costs. In China, while the upstream acrylonitrile market prices remained relatively stable, but rising acetone costs resisted MMA production between March and April. However, affected by shutdowns for maintenance in the USA and Europe during February to April, a gap in overseas demand appeared, leading to a year-on-year increase of 30~40% for export orders. Conversely, MMA makers increased their production slightly, with MMA operating rates increasing by 10% to approximately 60~70%, considering poor domestic market demand and high acetone costs. It’s heard that Shenghong Group, Jiangsu Sierbang Petrochemical Co., LTD 340kpta MMA plant in Lianyungang, plans to shut down one line in March. It’s said that Jiankun 150kpta MMA plant in Jiangsu, restarted in March and is running at approximately 60%. Reports indicate that Zhejiang Petroleum & Chemical 180kpta MMA plant in Zhejiang, Zibo Qixiang Tengda chemical co., Ltd 200kpta MMA plant in Zibo, and Dongming Huayi Jade Emperor New Materials Co., Ltd. 50kpta MMA plant in Shang Dong, are under plans to shut down. It’s heard that Liaoning Kingfa’s 260kpta acrylonitrile(AN) plants to shut down for maintenance, in line with a 100kpta MMA plant shut down in January. Influenced by current poor market demand and escalated geopolitical tensions, it’s difficult to justify acrylonitrile (AN) production. HCN supply situation is not improving, and the same is true for MTBE and acetone prices, which hovered at high level, dampened by overall market supply constraints persisting due to limited increases in operating rates. For the reason, MMA average running rate stable at 60~70%.